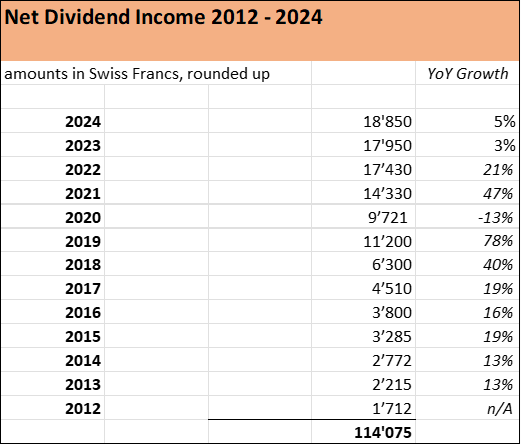

I’ve been building my dividend stock portfolio for almost 14 years now and as you can see, the dividend income increased quite nicely year by year. Of course, there have also been some setbacks, for instance in 2020 during the COVID pandemic, several companies cut their shareholder payouts. But all in all, the compound effect really shows, fueled by a combination of

dividend increases (“organic dividend”)

dividend reinvestments and

addition of new stock positions or increasing existing share positions

As of today, my stock portfolio has a market value of well above USD 650’000, almost 35 % consists of tech companies and only a few pay dividens such as Meta, Alphabet, Microsoft, Apple, NVIDIA, Prosus and ASML. Insurance businesses (Swiss Re, Münchner Rück, Zurich Insurance, Legal & General etc.) and resource companies (Chevron, EXXON, BHB, Rio Tinto etc.) have been the main dividend contributors for the last years.

The main reason for slower dividend income growth in the last two year were significantly lower savings rates in 2023 (18 %) and 2024 (12 %) which led to lower investments into publicly traded stocks compared to previous years. I have also reduced historically strong European dividend payers over the last 18 months and shifted the focus more on US tech stocks. As said, most of them don’t pay dividends but offer great growth opportunities.

Adding interest income (from bank savings, bonds and Peer to Peer investments) of around USD 2’000 to my total passive income in 2024 total net revenue stood well above USD 20’000, covering around 30 % of the total annual spendings (rent, grocery etc.) of our family of four.

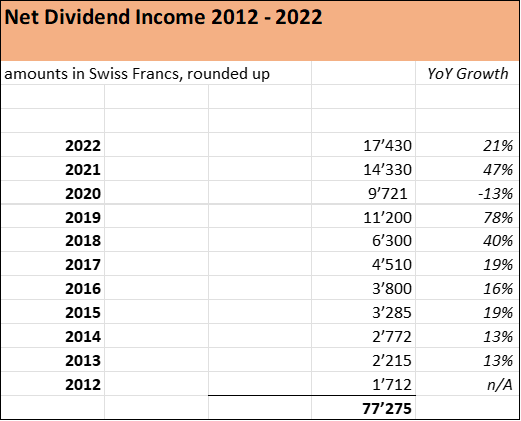

My full year 2022 dividend review is more than due.

2022 has been incredibly dynamic and I have been extremely busy building and growing my own consulting business I started early last year. I am extremely happy that my company is doing very well. Our savings rate however fell quite significantly. While in 2021, our savings rate stood at around 65 %, it was around 10 % in 2022. My business turned into profit pretty fast, but my income has been lower in 2022 than in the previous years. So, our investment process slowed quite a bit, but I still managed to save a decent amount of money to put to work and last year I bought stocks of strong businesses like Mondelez, Hershey, Visa, Nike, ASML etc. strengthening our investment portfolio further.

It was in 2016 that I started this blog to document our Journey towards Financial Independence by 2024. Our initial plan back then was to build a sizeable dividend stock portfolio plus further investments covering our annual spendings which range from around USD 50’000 to 55’000 annually. As you can see from this update, there is still a long distance to go. But what’s clear: dividend growth investing really works. After a few years, the power of the compound effect really shows. And our passive income maching slowly but surely is gaining more and more steam.

USD 20’000 passive income in 2022

In 2022, total dividend income was 17’430 Swiss francs respectively over USD 19’000 (one Swiss francs corresponds to around 1.1 USD). We also had some additional passive income from Peer to Peer Investments and from corporate bonds plus interests on our savings accounts. Altogether, these interest income streams amounted to around USD 1’000. So grand total, our passive income amount was around USD 20’000. That’s quite significant. Let’s put it that way: one third of our annual spendings of our family of four is covered by passive income!

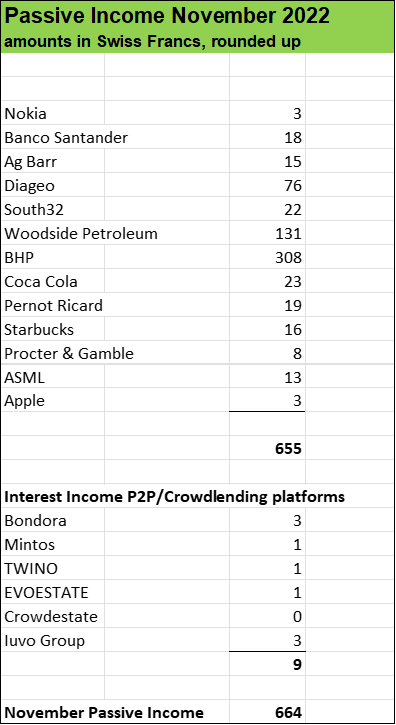

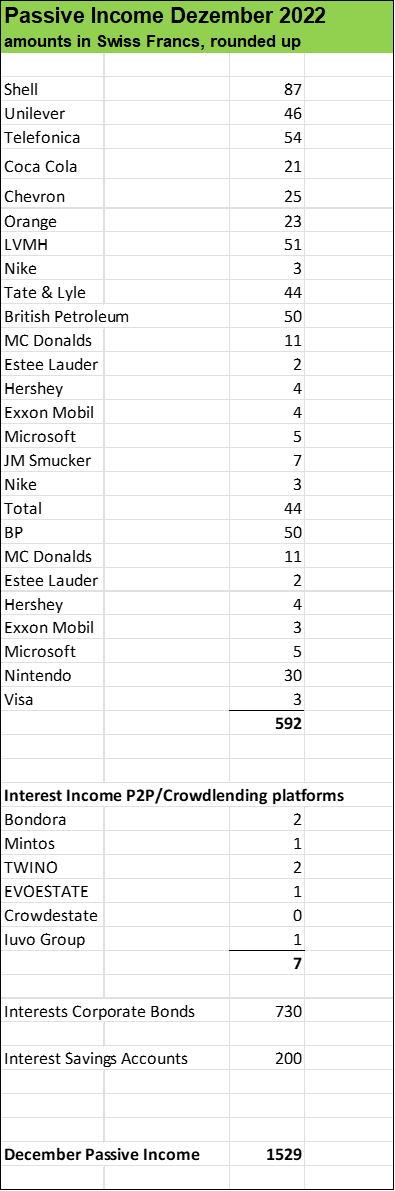

Now, let’s quickly go through some numbers. Here’s the update of the last two months in 2022 (November and December):

Compared to November 2021, there was a massive increase of over 50 % on the back of hefty dividend payments of mining company BHP Billiton and oil giant Woodside Petroleum.

As my consulting business has turned into profit, I also incrased my salary. And as my income has incrased significantly over the last few months, I am now able to step up my investment process quite significantly.

Targeting passive income of over USD 20’000 for 2023

Since 2012, cash flow generation of our dividend stock portfolio has been growing quite strongl due to a combination of following factors:

dividend hikes (organic growth)

dividend reinvestments

addition of new positions and increasing existing holdings by putting new funds (savings) to work

Over the next months I plan to invest at least USD 50’000 into our investment portfolio which currently has a market value of roughly half a million.

Our initial plan was to achieve Financial Independence by the end of 2023. It might take a few years longer. But that’s completely fine, we keep enjoying our path and we have so much flexibility in life.

For the time being, we stick to our initial plan and continue to work hard, save a as much cash as possible which is fueling our consistent investment process.

The Pursuit of Financial Independence had so many positive effects in our life.

For instance, I left the corporate treadmill and started my own business which has been a dream for quite a while.

We have built a nice portfolio consisting of strong income generating assets and we also a very nice cash pile. It’s great to have options in life and not having to rely on a job or a boss. That’s just a few of the huge benefit of pursuing Financial Independence.

Take care, fellow reader, and thanks for your interest in our journey.

2022 has been incredibly dynamic so far and I have been extremely busy building and growing my own consulting business I started early this year. This dividend update is more than overdue, in fact it has been half a year since I’ve published my last passive income update. Sorry about that.

I hope to be able to return to my monthly dividend updates very soon. I’ve been doing so for more than six years, since 2016 when I started this blog to document our Journey towards Financial Independence by 2026.

We are still working towards that goal and in fact having been streamlining our finances and establishing various passive income sources for years certainly played some role in my decision to start my own business.

From January to October, grand total of our our investment portfolio net income was USD 16’000, an increase of 60 % compared to the previous year. That corresponds to a big chunk of our fixed cost block.

So, without further ado, let’s have a look at the last six months in terms of passive income, starting with October.

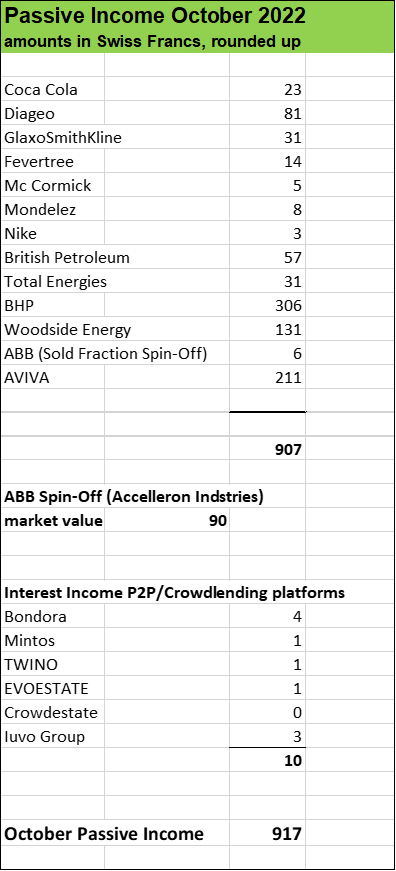

October showed a nice 26 % passive income jump on a year over year basis

Compared to the previous year with USD 725 in passive income, October 2022 showed higher amounts due to a combination of

organic dividend growth

dividend reinvestments plus

added or increased stock positions (Nike as well as Woodside Energy, a spin-off of BHP Billiton).

As you can see, commodity, resource and oil businesses (British Petroleum, Total Energies, BHP, Woodside Energy) as well as insurances (AVIVA) make up for the bulk of my passive income contributions not only in particular to this month but with regard to the portfiolio in general.

What’s also worth noting that new shares of existing position ABB – called Accelleron Industries – have entered my portfolio with a market value of around USD 90. Spin-Offs are pretty nice additions, for instance in the case of BHP Billiton, two separated companies – South32 and Woodside Energy – made interesting additional dividend payers.

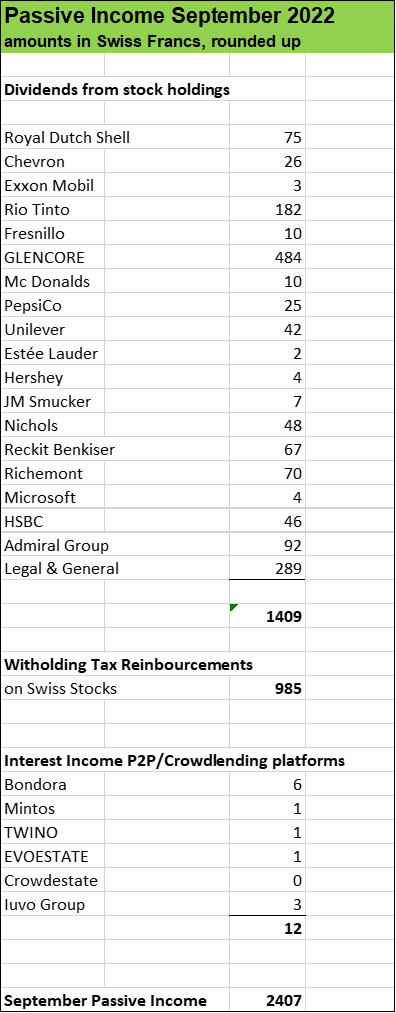

September dividend income in line with previous year

September 2021 was already a strong month with around USD 1’460 in dividend income. This year, it was more or less the same amount generated by dividend paying stock positions.

However, in particular on the back of witholding tax reimbursements in the amount of USD 985on Swiss stocks such as Nestlé, Roche, Novartis etc., September became a particularily strong month.

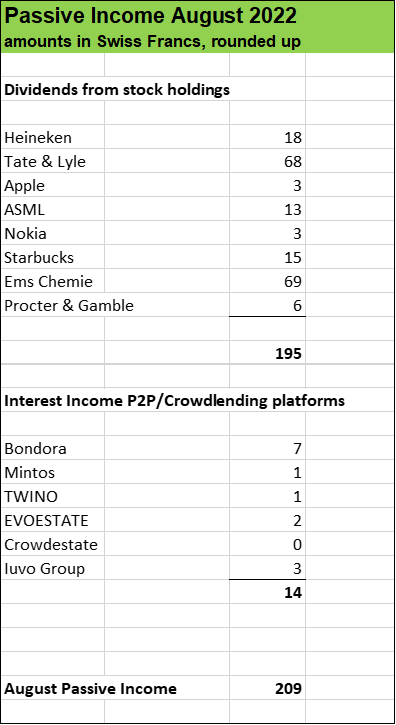

August showed a passive income increase of 38 %

Early in 2022, I added three new stock positions which contributed nicely to our passive income stream:

Starbucks

Ems Chemie and

Procter & Gamble

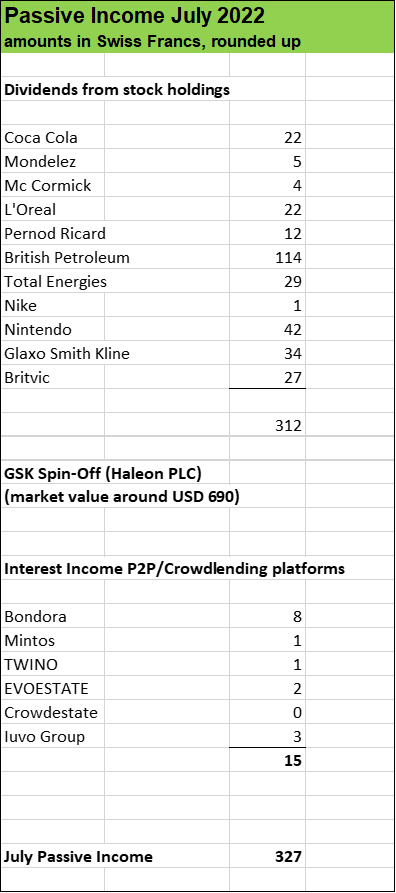

July passive income was pretty in line with the previous year

While there was some nice organic dividend growth in the case of Coca Cola, Mc Cormick and L’Oreal as well as positive effects from dividend reinvestments, overall total passive income was more or less in the same range as in the previous year due to significantly lower interest income from Peer to Peer investments which I have been further reducing for many months.

It’s worth noting that pharmaceutical company Glaxo Smith Kline (GSK) made a spin-off. The new shares of Haleon I received had a market value of around USD 690 at the time of the distribution and I will keep this position. Sometimes, spin-offs can make interesting positions over time (see BHP which separated South32 for example).

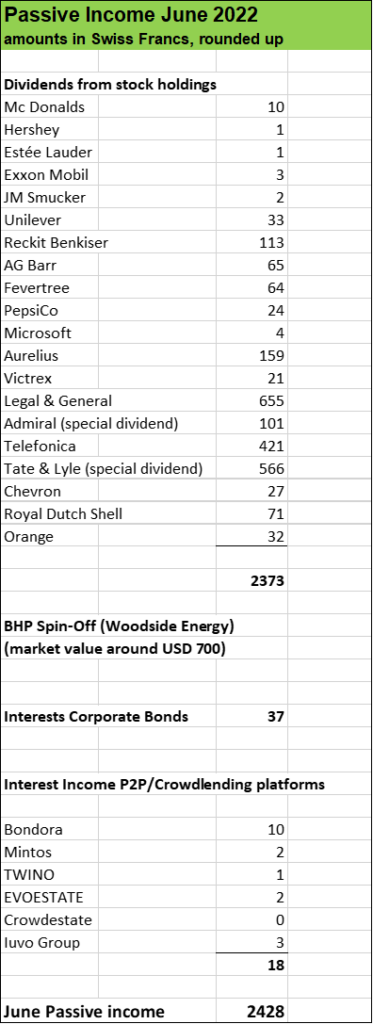

A very cool 100 % passive income jump in June

June showed some very positive effects in form of special dividends (Admiral, Tate & Lyle). Furthermore,

dividend reinvestments (Legal & General, Royal Dutch Shell etc.) and

new stock positions (Hershey, Estée Lauder etc.)

contributed to the overall income jump.

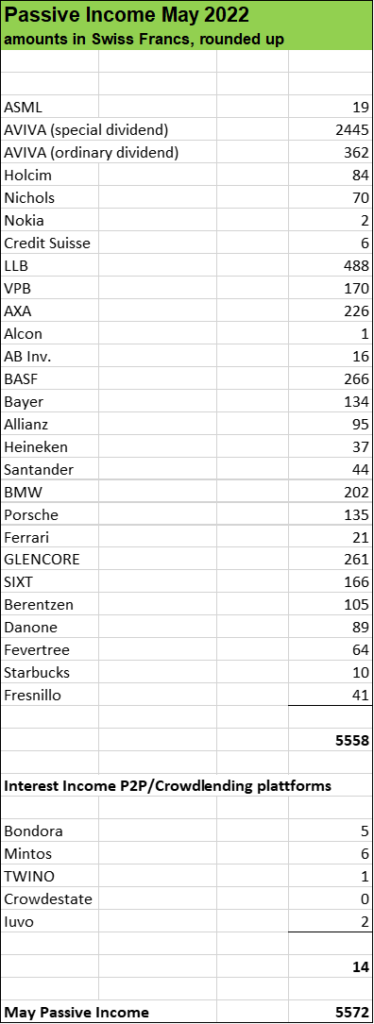

50 % higher passive income in May

On the back of a huge special dividend from UK insurance giant AVIVA in the amount of over USD 2’400, May showed a very strong month. In fact, in that month, my passive income considerably exceeded our household spendings which is always a very nice thing to see.

What about you, fellow reader, have you added some stocks to your portfolio recently? How is your passive income developing

Disclaimer You are responsible for your own investment and financial decisions. This article is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

Retirement planning is a process that involves multiple steps, each evolving as you grow closer to your retirement. If you want to have a comfortable, fun, and financially secure retirement, you need to start planning it now. Here are seven steps you should take, no matter your age, to build a solid retirement plan.

This is a guest post. Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning firm based in Goodyear, AZ. See the Author Bio below the article.

7 Steps to Building Retirement Wealth

Reaching your retirement goals might take longer or sooner depending on your income and the challenges you face throughout your life. But you’ll get there if you take these seven things to build retirement wealth. So, here they are:

1. Invest in Your Health

With age, your medical costs increase as you become vulnerable to many lifestyle diseases and chronic illnesses, including high blood pressure, arthritis, high cholesterol, and heart diseases. Although some health conditions are inherent and beyond our control, there are others that can be controlled and treated through regular screenings, proper medical care, and a healthy lifestyle. Investing in living a healthy life is always better than spending a fortune on medical treatments.

2. Create a Budget

Most people who retire as millionaires create a budget and stick to it. There is no magic pill that can make you a millionaire overnight. If you want to build wealth, you have to plan for it, and creating a budget is the foundation of any money-saving plan. So, sit down every month to create a budget and allocate funds for each of your expenses, investments, savings, and financial goals.

3. Save for Retirement

Once you have set aside money for retirement, it’s time to invest in retirement accounts like a self-directed IRA and a self-directed 401(k). These accounts help you live an independent retired life and also cover emergency costs during retirement.

4. Maximize Your Social Security

Most people live past their “break-even point.” This can be concerning because the longer you live, the greater are the chances of you running out of your savings in retirement. However, you can make your money last longer if you decide to delay taking your Social Security benefit as long as possible. So, when you run out of your savings, you can then depend on your Social Security checks to serve your longevity.

5. Increase Your Income

Consider having multiple income streams to build your wealth. Some of the ways to increase your income include: venturing into business, taking up a part-time job, running a side hustle, etc.

6. Consult a Tax Expert for Advice

If you have been a good saver, you might be thrown into a higher tax bracket in retirement. A higher income in retirement can also have tax implications on your Social Security benefits and increase your Medicare premiums. The math involved can be complicated and intense. So the best way to reduce your tax burden in retirement is to consult a financial expert.

7. Keep Your Debt in Control

The only good debt you can have is no debt at all. When you spend your income and savings on loan payments, you’ll have less money at your disposal to save and invest. So, it’s important to manage debt and use proven strategies like the snowball method and the avalanche method to get rid of debt. Most importantly, after you get out of debt, make sure that you work doubly hard to stay out of debt. Sooner or later, retirement is coming. Being financially prepared for it is the best way to ensure a comfortable, fun, and secure retirement. Start your journey with the above retirement wealth-building steps. With dedication and discipline, you will be able to see your wealth grow faster than you had imagined.

Author Bio:

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning firm based in Goodyear, AZ. He regularly writes for his own blog of Self Directed Retirement Plans and as a guest blogger to many sites in the niche of finance.

If you need help and guidance with traditional or alternative investments, email him at rick@sdretirementplans.com or visit www.sdretirementplans.com.

Disclaimer You are responsible for your own investment and financial decisions. This article is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

My new created business had a good start and we continue working hard towards Financial Independence

Hey there fellow reader. It’s been quite a while since I’ve published a new posts. In fact it has been four months since I’ve published my last passive income income update. Sorry about that!

I’ve been documenting our journey towards Financial Independence since September 2016 and for over six years I’ve consistently reported on a monthly basis our progress we made in terms of streamlining our finances and establishing passive income sources.

However, the last few months have just been just so incredibly dynamic and it’s just now that I have been able to take a breath and write this post.

As I’ve written in some of my previous posts, I quit my job early this year to start my own business. It was a tough and risky move to leave my well paid position to do something I feel really passionate about and build a company providing e-learning and consulting services.

And I am so glad to say that this was the right move. My company started well and I’ve been able to win clients. I can see a healthy demand for my services.

Of course, there is a massive amount of work to do and to invest, in order to bring my company to the levels I want it to be.

In fact, if I hadn’t followed that path towrds Financial Independence, focusing on a down to earth lifestyle and investing regularily our savings for almost 15 years, my guess is that I would not have had the courage to leave my job and follow my dream. When it comes about Financial Independence it’s that process that is extremely empowering, it is about gaining flexibility in life, creating options and steadily building a strong position to reduce the dependency of a job. And of a boss.

So, without further ado, let’s have a look at the past four months, on how my dividend payers have developed compared to the previous year.

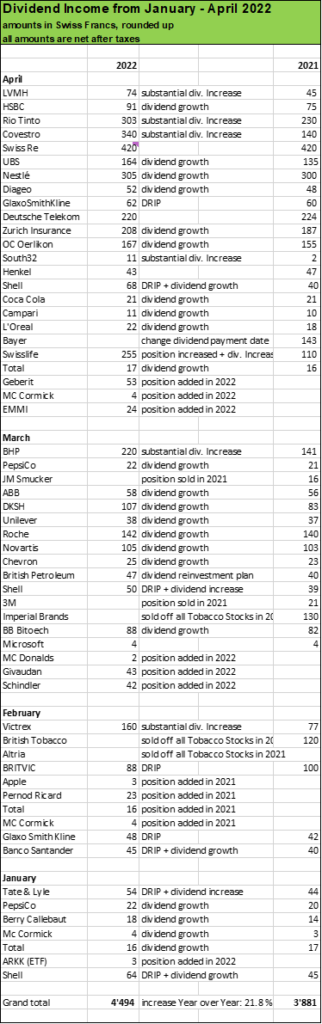

From January to April, our cash flow from Dividends climbed almost 22 % year over year

Over the first four months in 2022, roughly USD 4’500 have been generated from stock holding distributions compared to USD 3’800 in the preivious year. All these numbers in the chart below are in Swiss francs, which trades more or less at parity to the USD. The numbers are all net amounts after taxes. Witholding tax reimbursements are reported separately in my passive income updates.

When looking at the last four dividend months, the picture is very pleasing, showing healthy growth almost across the board.

Mining companies like BHP and Rio Tinto have been particularily strong but also the defensive positions like Nestlé, Unilever, PepsiCo, Coca Cola did not disappoint. Slowly, but steadily, my dividend generating stock portfolio is transforming into an strong cash churning compounding machine.

My plan for 2022 is to achieve at least USD 16’000 which is roughly 15 % higher than in the previous year. This goal should be pretty achievable through a combination of

organic dividend growth of most of my stock positions

special dividends in particular from share holdings in the commodity sector

dividend reinvestment plans (DRIPs)

addition of new share positions as well as doubling down on existing stock holdings

On the other hand I disposed off all my tobacco shares (Altria, British American Tobacco, Imperial Brands) in 2021 and this move alone reduced my dividend income potential by almost USD 1’000 per year.

Furthermore, exchange rate fluctuations have been a drag. The Euro for instance lost almost 6 % against the Swiss francs in the last few months. The British Pound devalued as well against the Swiss francs.

However, a strong Swiss francs has been good for me, it makes international stocks cheaper. And amid hightened volatility in the stock market to be expected for at least the rest of 2022, there will be several buying opportunities to strengthen our stock portfolio even further.

What about you, fellow reader, have you added some stocks to your portfolio recently? How is your passive income developing?

Disclaimer You are responsible for your own investment and financial decisions. This article is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.